The conflict in the dry bulk trade market

a positive outlook for dry bulk market is a deterrent factor that discourages owners from scrapping, but if it has led to new orders, it will definitely make the supply side even stronger, and this time the high fuel costs will help to make other recession.

According to MANA correspondent, analysts in their reports announced that by imposing customs duties on the imports of steel and aluminum from China by the US government and in turn imposing tariffs on soybeans from China, the dry bulk market will experience turbulences. This will occur because of the possibility of compensate not only from China but from other countries in Europe as well as Asia. At present, these conflicts keep the level of trade at the lowest levels.

No doubt, China has an important and significant role in the dry bulk trade market, so any changes in its policies and between it and other countries, or any program and law within the country, directly or indirectly, will affect the trade of dry bulk. The Chinese government's decision to apply a 25% tariff on the import of soybeans from the USA will change the trade route of importing this product into Brazil and Argentina. By this way, demand of tonne-mile for Panamaxes, Supramaxes and Handysizes will increase. On the other hand, the USA decision to impose tariffs on imports of Chinese industrial goods to encourage domestic production will damage the tonnage demand for major raw materials.

In a report, Banchero Costa researching group noticed that in 2017, China imported 5 million tons of sorghum from the USA, but the import will drop substantially by 2018, as much of the demand for sorghum will be supplied from the eastern coasts of South America, the Mediterranean and the Black Sea regions. Trump’s government signed an agreement of imposing new tariffs on imported goods from China which valued $60 billion. These tariffs will intensify uncertainty in dry bulk market. The positive and negative effects of this act will reveal in the medium term, but the share of Losers and winners seem to be equal. In the following lines, the various parts of the dry bulk market will be reviewed.

Ø Coal and iron ore

China’s Belt and Road Initiative (BRI) which was previously called "One Belt, One Road” can flourish dry bulk sector in the long term. The Chinese government is planning to invest in infrastructure development to build the 16th-century Silk Road which connects China to Central Asia and the Middle East to Europe, creating a maritime link between China and Southeast Asia to East Africa. BRI will consist of constructing new structures such as ports, roads, railways, power plants and pipelines. Up to now, estimated cost of the project has been $ 8 trillion by 2020. Restricting the activity of coal and iron ore mines in China, along with its efforts to reduce environmental pollution, will require the country to meet its needs of this sector by import. In this regard, Brazil and Australia are the main exporters of iron ore to China, and so far, high quality coal is imported to China from Australia, USA, South Africa, Colombia and other exporters around the world, which according to China's policies, these imports will increase, and in turn it will increase the tonne-mile index and make a boom in the bulk shipping market.

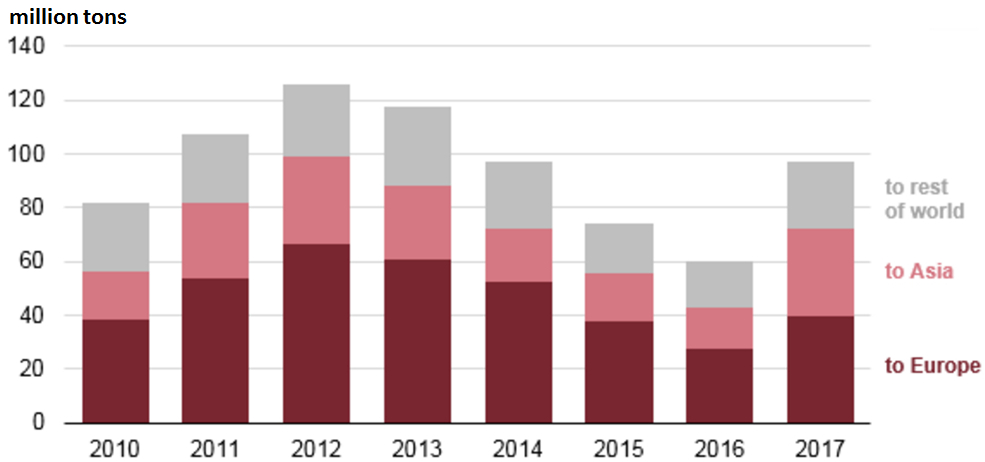

In 2017, aggregated coal exports of USA was 97 million tons, which has 61% growth compare to 2016. Exports to Asia have been more than doubled from 15.7 million tons in 2016 to 32.8 million tons in 2017, although European countries remain the largest destination for exports from the USA. If other countries cope with the policies of USA about imposing tariffs on foreign goods in support of domestic production, its coal exports will surely be on the downward trend like the five-year period previous to 2017.

No doubt, China has an important and significant role in the dry bulk trade market, so any changes in its policies and between it and other countries, or any program and law within the country, directly or indirectly, will affect the trade of dry bulk. The Chinese government's decision to apply a 25% tariff on the import of soybeans from the USA will change the trade route of importing this product into Brazil and Argentina. By this way, demand of tonne-mile for Panamaxes, Supramaxes and Handysizes will increase. On the other hand, the USA decision to impose tariffs on imports of Chinese industrial goods to encourage domestic production will damage the tonnage demand for major raw materials.

In a report, Banchero Costa researching group noticed that in 2017, China imported 5 million tons of sorghum from the USA, but the import will drop substantially by 2018, as much of the demand for sorghum will be supplied from the eastern coasts of South America, the Mediterranean and the Black Sea regions. Trump’s government signed an agreement of imposing new tariffs on imported goods from China which valued $60 billion. These tariffs will intensify uncertainty in dry bulk market. The positive and negative effects of this act will reveal in the medium term, but the share of Losers and winners seem to be equal. In the following lines, the various parts of the dry bulk market will be reviewed.

Ø Coal and iron ore

China’s Belt and Road Initiative (BRI) which was previously called "One Belt, One Road” can flourish dry bulk sector in the long term. The Chinese government is planning to invest in infrastructure development to build the 16th-century Silk Road which connects China to Central Asia and the Middle East to Europe, creating a maritime link between China and Southeast Asia to East Africa. BRI will consist of constructing new structures such as ports, roads, railways, power plants and pipelines. Up to now, estimated cost of the project has been $ 8 trillion by 2020. Restricting the activity of coal and iron ore mines in China, along with its efforts to reduce environmental pollution, will require the country to meet its needs of this sector by import. In this regard, Brazil and Australia are the main exporters of iron ore to China, and so far, high quality coal is imported to China from Australia, USA, South Africa, Colombia and other exporters around the world, which according to China's policies, these imports will increase, and in turn it will increase the tonne-mile index and make a boom in the bulk shipping market.

In 2017, aggregated coal exports of USA was 97 million tons, which has 61% growth compare to 2016. Exports to Asia have been more than doubled from 15.7 million tons in 2016 to 32.8 million tons in 2017, although European countries remain the largest destination for exports from the USA. If other countries cope with the policies of USA about imposing tariffs on foreign goods in support of domestic production, its coal exports will surely be on the downward trend like the five-year period previous to 2017.

US coal exports by destination 2010-2017

Clarksons predicts that in 2018, coke coal trading will increase by 4%, and iron ore trading will increase by 3%, compare to 2017. By considering that iron ore trade concentrates on long-term contracts of Capesize carriers on Brazilian and Australian routes to China, and its revenues are increasingly unstable, ship owners are always seeking to diversify their services to achieve their goals and sustainability.

In the whole, despite the challenging environment, iron ore and coal trade market will not have a gloomy future, as there is always a huge demand for them from a country like China.

Ø Grain

It is predicted that global grain trade will continue to grow steadily over the next decade. After a decade of sustainable growth, due to environmental changes, as a bright spot in dry bulk perspective, grain trade has attracted the attention of many ship owners.

Although iron ore and coal are the main areas of bulk trade, the booming trade of grains in the past has been a major source of revenue for ship owners and operators, especially for Panamax vessels on long trade lanes and for ships with cranes in regional cargoes. The increase of demand for grains in the African and Asian countries will also boost the grain market.

According to the Clarksons, the compound annual growth rate[1] (CAGR) of grain trade (including soybean, wheat and coarse grains) over the last decade amounted to 5.3%, which was the second largest in all dry bulk trades after iron ore.

In recent years, Pan Ocean and Bahri have announced that they have a plan for expanding the grain trade through the intermediaries, while Star Bulk has established a logistic center in Genoa to get closer to grain charterers. These measures suggest an annual growth rate of 3 to 4 percent over the next five years, according to Cargill.

IGC[2] has predicted the grain trade in the 2022-23 to reach 555 million tons. These data take into account some of the hypotheses, such as population growth, trade and agricultural policies, and forecasts for the global economy, but do not consider weather-related disruptions. This council also added in its recent report that soybeans play an important role in this increase: "Given the increasing demand in Asia and Africa, global trade is expected to peak in all four cereal sectors."

In addition, the IGC expects the trade of grains reach to 172 million tons in the 2022-23 from 145 million tons in the 2016-17. The Council, pointing out that Brazil will be the largest grain exporter, added: "Given that China's imports will account for two-thirds of the total grain trade volumes in 2022-23, the growing demand of Asia will continue to increase trade volume over the next five years."

According to the experts in this area, the impact of tons-miles will be even greater as the volume of supplies from the South of the USA is still rising. So, the trade of grains can be analyzed separately in two main parts as follows:

Ø Soybeans

Clarksons has predicted that soybeans will have a very good 5% growth compare to 2017 and reach to 155 million tons in 2018. This is the largest growth rate among all major dry bulk cargoes. According to CEO of Pacific Basin, soybeans will have the most grow. During the last decade, growth in this sector was 7% - 8% compare to wheat and coarse grains which had 4% increase during the same period. The motivator of this growth is the change in food habits and the consumption of more meat, especially pork, in the world. This leads to the massive transport of soybeans as feed from South America to China and other parts of Asia.

Ø Wheat and coarse grains

With regard to the steady growth in imports of Europe and the Middle East, especially in Saudi Arabia and Iran, Clarksons predicted that global trade of wheat and coarse grains would increase by 2% in the 2017-18 to reach around 359 million tons. It has also estimated that imports to the Middle East will increase by 9% to 60 million tons, and it will account for 85% of the global grain trade growth.

Reduced wheat production in the United States and Australia will be offset by Russian suppliers. Through favorable weather conditions in Russia, exports from this country will increase by 17% to 42 million tons, but the infrastructure constraints will limit this growth in the future. Some media have announced Russia's decision to increase exports to the Middle East and Latin America. This country currently exports to Turkey and Egypt.

Clarksons predicts that in the next year, South American wheat and coarse grains production is also very good, with more than 50% increase over the previous year, it will reach to 60 million tons. This is due to more competitive prices than the USA.

The Effects of Draught and Global Warming on Bulk Trade

Experts believe that the global climate phenomenon will diminish the supply of food and water globally and will affect the global economy as well. Colombia, Pakistan, Somalia, Australia, Guatemala, China and Kenya are just some of the countries that suffer from severe drought conditions.

When talking about water as food and drink, its sources of supply are unlimited in the world and should only be managed globally. Now the global drought has had a profound impact on the economy. In fact, water scarcity affects the location of business, and as a result, the more water resources, the more production and agriculture. So, such countries will overcome the nations that are in shortage. This leads to limited economic growth. The drought has been hurting earth for centuries, but some believe that this time the drought is different from the past, and because of this, we will see more floods and droughts in the decade ahead. The global warming leads to changes in location, time and quantity of rainfall, and these changes mean the supply of agricultural products from some parts of the world to the other parts are different.

So, droughts impose huge costs on world economies. The World Economic Forum (WEF) has estimated annually drought costs around the world at $6 to $8 billion due to losses in agriculture and related businesses.

The trade can help to solve the drought problem. There are plenty of arable land and enough water worldwide to produce demanded foods. The drought in some countries of the world will make profit for farmers in countries that do not deal with the water crisis. As a result, countries such as Argentina, Canada, Brazil and the United States will benefit more from exporting their agricultural products to countries suffering from water scarcity. Therefore, weather conditions will lead to weaken of the economy, but will generally contribute to the prosperity of bulk trade globally.

Bulk Carriers’ revenue: Something Better than Nothing!

Drewry had anticipated that bulk carriers’ rates would improve from the second quarter of 2018, because of increasing iron ore demand in Asia. In the medium to long term, it had provided a similar perspective in its previous research. With the widespread construction activities of China in the "One Belt, One Road" project, steel consumption will definitely increase. At the same time, the Chinese government has stopped unproductive mines with high contamination levels, so it will pave the way for more efficient mines to produce steel with better quality and will increase the demand for high quality imported iron ore.

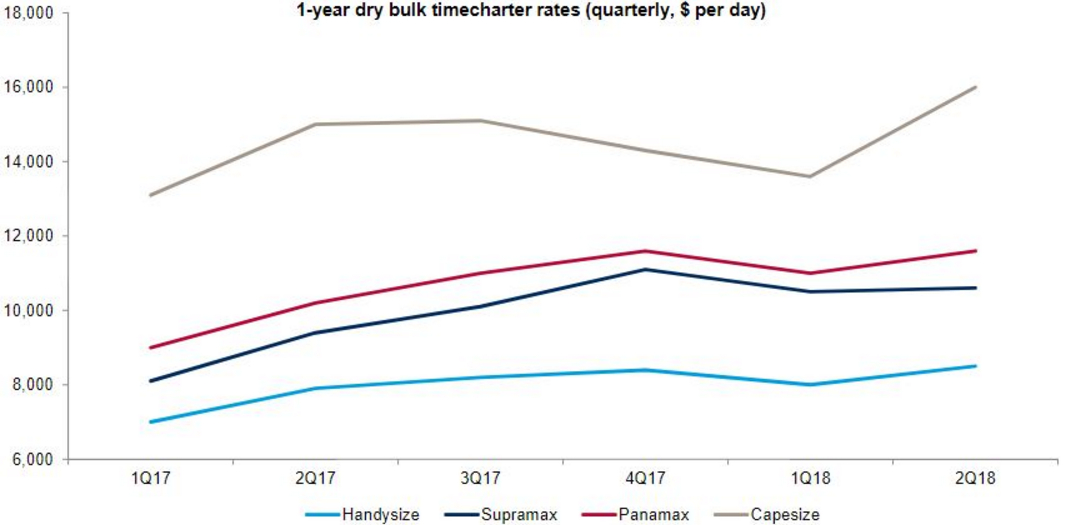

Compared to the Capesize section, the smaller carriers sector will have more chance for making more money in 2018. After 2 years being in peak, Panamax and Supramax revenues reached to around $14,000 per day in March 2018, compensating for more than 70 of the drop from average in early 2016. The Handisize division also had a major improvement, and the average of daily earnings reached to $ 10,882 in March 2018, and offsetting 80% of the reduction of the average before the recession. Totally, smaller carriers section has taken benefit of the growth of coal, grain and minor bulk trade during 2017.

Therefore, even though the Capesize market has suffered a seasonal breakdown, the average revenues in the bulk sector have offset more than half of the historical drop in the average level. Although there is still fluctuation in the way of market rebalancing, it looks as if since 2016 (the year of the most declines in bulk shipping rates), this sector has been improving. Lloydslist predicted in its analysis that the freight rates of bulk carriers will continue to increase in 2018, while fleet growth will be at its lowest level in the last ten years.

A decade has passed since when dry bulk rates began to decline in 2008. The long recession, which coincided with the financial crisis, peaked in January 2016. While many withdrew in the harsh market situation, a quick look at the BDI shows how drastic was the price fall and how moderate is this improvement. The dry bulk market has never returned to pre-recession conditions. In 1999, the average BDI was 1338 units. While in late 2017, by the comprehensive management, it reached the level of 1,500 units, and at many periods of time in 2017, it was lower than the levels in 1999.

Confusion in Dry Bulk Carrier Shipping

Now nobody is looking for a return to the past, and owners and dry-bulk activists are only happy to manage their business without loss. Now, how the bulk section in 2018 relates to the 1999 situation is an issue that is apparent when looking at numbers and figures. While the global fleet capacity has got to more than 3 times bigger than its size in 1999 which was 264 million DWT, and reached to 817 million DWT in the first quarter of 2018, bulk carriers are less efficient and carry less. In the period from 1999 to 2008, in average approximately 8 - 9 tons of freight had been carried by per DWT but since 2009 this average has dropped to 6 - 8 tons per DWT. Of course, the demand for bulk cargo transportation has increased from 2,155 million tons in 1999 to 5096 million tons in 2017, but this increase has not been as much as the growth of fleet capacity.

Clarksons in its recent analysis predicted that dry bulk freight rates will increase sharply over the next three years, as demand will surpass supply over this period. The new orders for Handysize, Handymax and Supramax, in particular the order for 40,000 – 45,000 DWT vessels, are at a low level. This particularly affects the transportation of shipments such as aluminum, bauxite, copper concentrate, manganese, chrome rock, zinc concentrate, sugar, cement, compact fertilizers and cereals. The supply of these ships will be limited over the next three years. While freight rates were at the lowest levels in 2016, they have increased by more than 200% over the past two years, but it has not yet returned to the flourish period before the 2008 crisis.

Dry bulk products have been increasing since 2000, with the exception of 2009 and 2015, it remained stable in 2015 compared to 2014 and did not increase. By 2017, seaborne trade of dry bulk was at the level of 5 million tons, but the freight rates rises were not impressive.

Since 2005, dry bulk shipments have grown 66%, while fleet capacity has increased by 86%. As a result, there is a surplus of capacity in the bulk sector, but the situation is expected to improve.

During 2017, new building orders for dry bulk carriers, especially smaller ones, were reduced, and so far, the shipyards have often delivered previous orders. The capacity of shipyards has declined for bulk vessels, especially in China. . In some cases, the yards have started to build tanker or other vessels.

Over the past six months, the new orders for bulk carriers have grown a bit, but if the trend of rising freight rates continues, then orders may increase and the improvement will not resume. In fact, if the owners have not learned from previous experiences, they can seed for the next recession.

Given the fact that politicians and governments often tend to support domestic products, they can have a huge impact on grain trade. Therefore, the US President's inclination to support domestic production could be considered the biggest risk in 2018. In analyzing the fleet, major issues are analyzed in following paragraphs.

Significant progress has been made in the field of efficient technologies, and at the same time China has much slower economy reveal only one fact: much of the capacity needs to be reduced! In fact, about 200 million DWTs, which include 30% of the active fleet capacity (equivalent to 5,000 ships with a capacity of 40,000 dwt), should be scrapped so that we can see the same rates as before 2008. Given the new orders, equivalent to 10% of the present fleet, large volumes of scrapping may be the easiest way to reduce capacity surpluses.

Owners should also cope with additional fuel costs. Fuel prices have risen from $100 per metric ton in 1999 to $380 per metric ton at present. Some other factors can greatly increase freight rates. 2020 sulphur cap will force ships to use low sulphur fuel. Although the shipping industry is not ready for the deadline (January 1, 2020), but if the owners of the ships have difficulty in providing low-sulfur fuel, they should choose alternatives such as installing scrubbers to subtilize exhaust gases. Some experts predict that the use of low-sulphur fuel would cost twofold compared to previous fuels. The largest share of the vessel's operating costs is related to the cost of the fuel, and the owner of the vessel will not be able to bear these costs, except to increase the freight rate. Consequently, the improvement in rates at the present should not be considered as a boom, and the situation would get worse by ordering new vessels.

The implementation of the International Maritime Organization's (IMO) 2020 sulphur cap is becoming increasingly important. Certainly there are constraints in the field of scrapping. The average age of the dry bulk carriers in the world has dropped from about 14.2 years in 1999 to about 8.8 years. However, owners who are facing the issue of lowering return on investment must upgrade their fleet.

The dry bulk market is also very fragmented, with many different partners from small independent companies to large government organizations. This leads to different views on market balance.

Overall, while the dry bulk market in 2017 saw a positive move forward, if the excess capacity problem is not resolved in this section, it will not be in the way of improvement. For years, we will not see a return to levels prior to 2008.

International Regulation: Solution or Problem?!

Owners have to comply with a set of laws and regulations such as the reduction of emissions and water balance management applied by the International Maritime Organization (IMO) and some governmental organizations. So, for fulfilling these requirements will require investment.

At the Singapore Shipping Forum 2018, which was held in cooperation with the Moore Stephens Institute and the BNP Paribas on April 26, it was stated that there is now much support for implementing low sulphur fuels rather than using scrubbers. Changing the fuel to low sulphur ones is not only a good work, it can also be positive for the market.

The simplest way to tackle the sulphur cap is to reduce speed. By reducing speed from 12 knots to 10 knots, it would effectively remove 17% of dry bulk shipping supply.

In general, ships of over 15 years of age, carrying a total of 142 million tons of cargo in the world, or 17% of the existing fleet, have the most potential for scrapping. Owners of such ships have to make a decision, as their older engines cannot burn low sulphur fuel oil and in addition, they would have to invest in ballast water treatments systems for such old ships which have their own problems.

Conclusion

Although weather conditions and policies in some countries, such as China, help boost trade, the shipping industry still faces a surplus supply. The relative prosperity of the market and the improvement of the freight rates are a dissuasive factor in scrapping, while international regulations, such as the 2020 0.5% sulphur cap and ballast water management, are a good incentive for scrapping of older ships. But we have to wait and see which of these two factors will be more powerful. If shipping companies act smartly and compare the rates with the years before the recession, they will not repeat the same mistake and know that this improvement is so fragile that it will make the situation worse with a small error. The solution at this time is just scrapping, while in March 2018 the amount of scrapping is estimated to be one fifth compared to March 2017.

In short, a positive outlook for dry bulk market is a deterrent factor that discourages owners from scrapping, but if it has led to new orders, it will definitely make the supply side even stronger, and this time the high fuel costs will help to make other recession.