Clarksons Describes Shipping Market

Clarksons observed tanker, bulkers and new building market meticulously in the first days of January 2018.

src="/files/fa/news/es/Thumbnails/19850b5f-ae08-40f0-a296-ac4c8b609ceb_260_199.jpg' class='img_convert' title='Clarksons Describes Shipping Market ' alt='Clarksons Describes Shipping Market '>

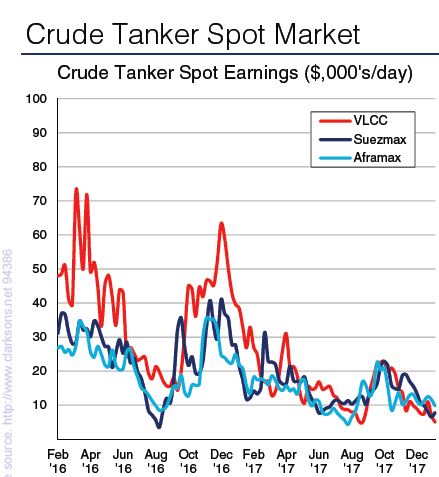

VLCCs

It has been a fairly uneventful week in the VLCC market. Although business has been concluded, there have beenno significant changes to rates across all the load regions. The battle for owners to overcome fundamentals and try to change sentiment is proving far too much to handle, and rates continue to bring sub-$10,000/day earnings. Going forward, it seems unlikely things will change much.

Suezmaxes

Following a bottoming out of rates midweek, the end of this week has seen resistance from owners to last done levels. prompt cargoes from the Black Sea to Med incited a firming in the rate on this route, which rose w-o-w to WS 67.5. The rate on the WAF-UKC route now sits at WS 55, up from WS 52.5 last week.

Aframaxes

The market softened in the North Sea/Baltic this week, and the rate on the Baltic-UKC route fell to WS 80. Elsewhere, rates on cross-Med routes fell w-o-w to WS 107.5.

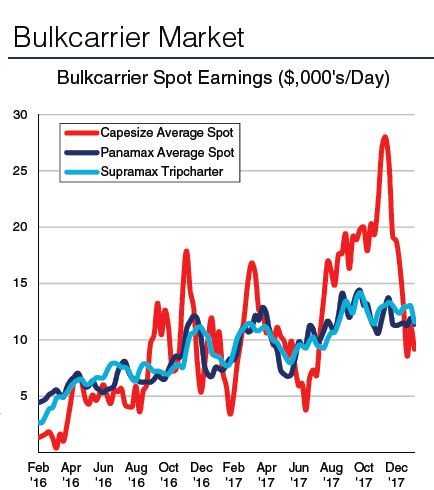

Capesize

Capesize voyage rates slid back across the board this week, with the spot rate on the Dampier-Qingdao route falling w-o-w to $6.25/tonne and the rate on the Bolivar- Rotterdam route falling to $7.90/tonne. Overall, average Capesize spot earnings fell 18% w-o-w to $9,165/day.

Panamax:

In the Atlantic, Panamax spot rates eased this week as a significant supply of available tonnage was able to absorb relatively limited supply of fresh minerals cargoes out of the USEC and Baltic. In the Pacific, spot rates softened asfresh cargo enquiry was limited, particularly in the north.

Handy

In the Pacific, it was an active week with sentiment turning slightly positive towards the end of the week, reflecting a steady supply of fresh cargo, although rates remained relatively steady. In the Atlantic, Supramax trip rates softened slightly, reflecting a lack of prompt cargoes particularly in the Med, and an oversupply of tonnage in the US Gulf and USEC.

Liner Market News

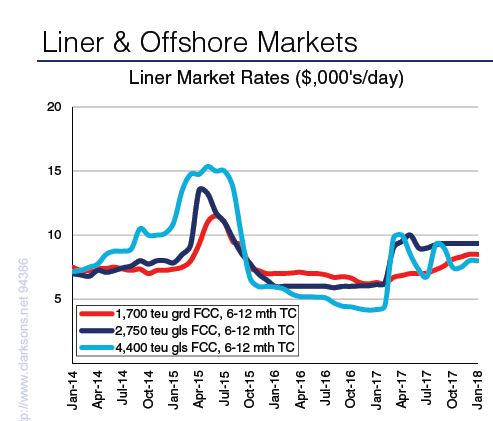

By the end of January 2018, containership charter rateassessments had generally risen m-o-m. Nearly all featured sizes recorded improvements relative to end 2017, while the idle fleet continued to shrink. In the smallersizes, the one year charter rate assessment for a 1,700 TEU containership rose 7% m-o-m to reach $9,400/day by the end of January, while the one year charter rate assessment for a 2,500 TEU containership picked up by 9% m-o-m to stand at $9,500/day. In the ‘old Panamax’ sector, the one year charter rate assessment for a 4,400 TEU containership increased by 9% m-o-m to reach $8,750/day, representing more than double the end 2016 level of $4,150/day.

• At the three key Asian ports of Shanghai, Singaporeand Hong Kong, container throughput in full year 2017 totalled 94.6m TEU, rising 8% y-o-y. Meanwhile, at the portof Jawaharlal Nehru, container throughput in January 2018stood at 0.42m TEU, up 13% y-o-y.

Shipbuilding News

In the bulker sector, 2020 Bulkers declared options for 4 x 208,000 dwt Newcastlemaxes at New Times SB, with the new units due for delivery in 2020. Foremost Maritime ordered 4 x 208,000 dwt Newcastlemaxes at Shanghai Waigaoqiao, with delivery due in 2H 2020 and 1H 2021. Beihai Shipyard won an order for 2 x 325,000 dwt VLOCsfrom U-Ming Marine, with the units due for delivery in 2020 and backed by a Vale COA. SK Shipping ordered 2 x 325,000 dwt VLOCs at Dalian Shipbuilding, also backed by a Vale COA, with delivery due in 1H 2021. Finally, M/Maritime ordered 2 x 60,000 dwt Ultramaxes at MitsuiSB (Tamano) and a 37,000 dwt Handysize unit at Saiki HI.

In the tanker sector, Pantheon Tankers declared options for 2 x 52,000 dwt MR product tankers at STX SB (Jinhae), with the new units due for delivery in Q4 2019.Meanwhile, Torm ordered 2 x 75,000 dwt LR1s at GSINansha, with delivery due in 1H 2020.• Elsewhere, SITC declared options for 2 x 2,400 TEUfeeder containerships at Jiangsu New YZJ, with delivery ofthe new units due in 1H 2020. Finally, NYK ordered a174, 000 cu.m. LNG carrier at Hyundai Samho. The unit is due for delivery in April 2020 and will go on charter to EDF.

Major Bulk Trades News:

China’s bauxite imports increased 39% y-o-y to 7mtin December, the highest volume imported into the country in nearly four years. This brought China’s total bauxite imports to 69mt in full year 2017, 32% higher than the volume imported in 2016. This rise largely reflects a more than doubling of imports from Guinea, with the country exporting 28mt of bauxite to China in 2017, becoming China’s largest supplier of the aluminium ore. Meanwhile, China’s soybean imports grew 6% y-o-y to 10mt in December 2017, with the country’s total soybean imports growing 15% y-o-y to 96mt in full year2017. China’s imports from the US rose 34% to total 33mtin 2017, while the country’s imports from Brazil also grew by 34% to exceed 50mt for the first time.