Clarksons Leafs Through the Last Week of Shipping Industry

Clarksons in its weekly report offered an analysis regarding tanker, bulker, demolition and newbuilding market.

src="/files/fa/news/es/Thumbnails/6eeec555-c70c-41d7-97e6-972cdff2a31b_260_199.jpg' class='img_convert' title='Clarksons Leafs Through the Last Week of Shipping Industry' alt='Clarksons Leafs Through the Last Week of Shipping Industry'>

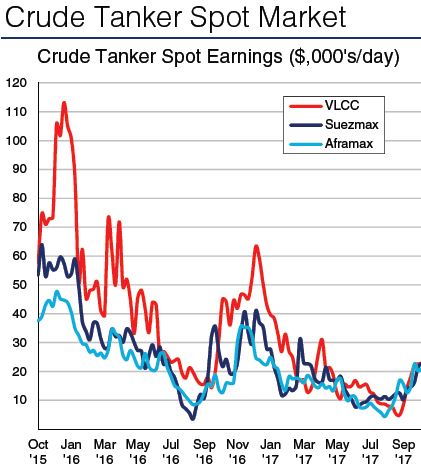

In the MEG, rates appear to have stopped climbing for now, but with a lack of modern tonnage, rates on MEG-East voyages are holding at around WS 70. The tone in the Caribbean market remains firm owing to limited tonnage availability, although activity has slowed slightly this week. With limited activity on MEG-West routes, owners may consider ballasting to the Caribbean if rates in the MEG fall.

Suezmaxes:

Rates jumped in WAF this week on the back of increased enquiry and a very tight tonnage list. The rate on the WAFUK Croute has increased by WS 12.5 to around WS 100.On the Black Sea-Med route, Turkish Straits delays and a tightening tonnage list have supported an increase in rates to WS 107.5. Sentiment remains firm going into next week.

Aframaxes:

Despite a stronger market in the Med, rates in the North Sea/Baltic region have eased back due to limited activity. It was an active week in the Med/Black Sea region, and with bad weather and increased Turkish Straits delays, rates on featured cross-Med routes have risen to WS 155.

Bulkers

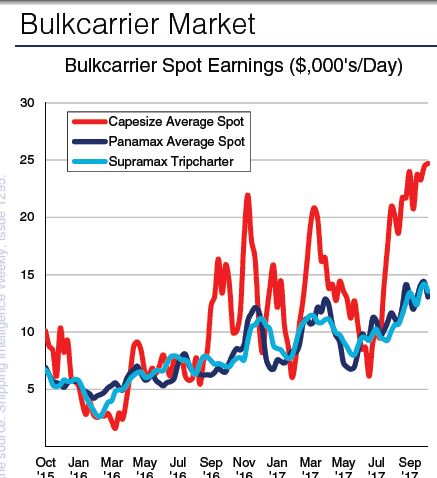

Capesize:

Weather disruptions at a number of Chinese ports continued to support Capesize spot rates in the Pacific early in the week, before easing as the week progressed. Overall, Capesize spot earnings rose 1% w-o-w to $24,717/day.

Panamax:

The Pacific market generally softened this week, with a widespread lack of cargo as well as a long tonnage list undermining Transpacific trip rates, although rates on backhaul routes increased firmly. In the Atlantic, activity was subdued with many players away at a major coal conference, and rates in the basin generally fell w-o-w.

Handy:

In the Pacific, sentiment was flat at the start of the week, and limited fresh cargo volumes across the basin exerted pressure on Supramax trip rates. In the Atlantic, increased tonnage availability in the US Gulf and reduced activity out of ECSA prevented rates from rising, whilst rates in the Continent remained steady.

Liner Market News

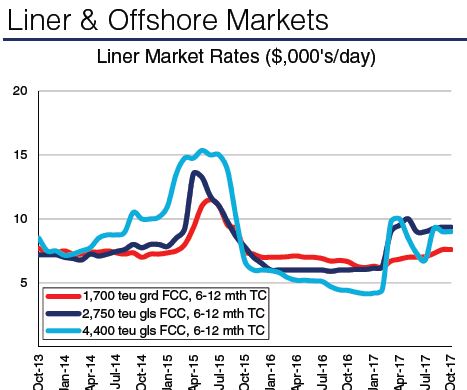

According to the Shanghai Containerized Freight Index, spot container freight rates on the peak leg transpacific route increased this week. On the Far East-US East Coast route, the spot rate climbed by 18% w-o-w, to stand at $2,075/FEU, whilst the spot freight rate on the Far East-US West Coast trade lane stood at $1,512/FEU this week, representing a w-o-w increase of 11%. Meanwhile, spot freight rates on the Far East-Mediterranean route remained relatively steady w-o-w, standing at $640/TEU.

Shipbuilding News

There are a number of newbuild contracts to report in the bulkcarrier sector this week. Korean owner Polaris Shipping has extended a series of 325,000 dwt VLOCs at Hyundai HI (Ulsan) by declaring an option for five additional units. The vessels are scheduled to be delivered between 2021 and 2022, and will become the 11th to 15th units in the series. Hyundai HI has also received an order for2 x 325,000 dwt VLOCs from Korea Line. The units are scheduled to be delivered from Q4 2019. In China, Jiangsu New YZJ has received an order from Zihni Group for 1 + 1 x 82,000 dwt Kamsarmax bulkcarriers.

The first vessel is scheduled for deliveryin June 2019. Meanwhile, Nova Shipping & Logistics declared an option for 2 x 64,000 dwt chip carriers at Chengxi Shipyard. The vessels are scheduled for delivery in 2019 and will become the 3rd and 4th vessels in the series. Elsewhere, Fujian Southeast SB has won an order for one 20,500 dwt bulkcarrier from domestic owner Fujian Yonghang. The unit is scheduled for delivery in 2019.

Major Bulk Trades News:

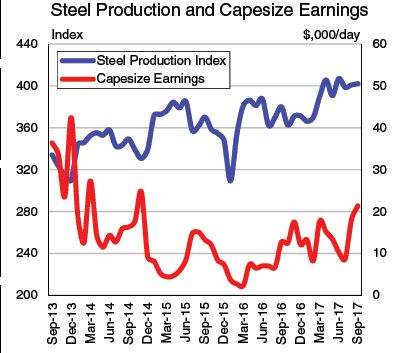

According to NBS statistics, Chinese steel production rose 5% y-o-y to 72mt in September, and increased 6% y-o-y to 639mt in the first 9 months of 2017. However, output in September fell 4% m-o-m and represented the lowest monthly level since February, reflecting the impact of recent measures to reduce air pollution over the winter. Chinese seaborne steam coal imports increased m-o-m for the second consecutive month to reach 19mt in September, up 14% y-o-y and representing the highest monthly total since November 2016. Import demand has been supported in recent months by tightness in the domestic coal market, with reports suggesting that recent environmental inspections led to a fall in domestic coal production to the lowest level in 10 months in August.