Most Recent Maritime News Updates Written by Clarksons

Clarksons in its weekly report offered an analysis regarding tanker, bulker, demolition and newbuilding market.

src="/files/fa/news/es/Thumbnails/70a8dddf-bd92-4d24-b7c1-15d8c82391ec_260_199.jpg' class='img_convert' title='Most Recent Maritime News Updates Written by Clarksons' alt='Most Recent Maritime News Updates Written by Clarksons'>

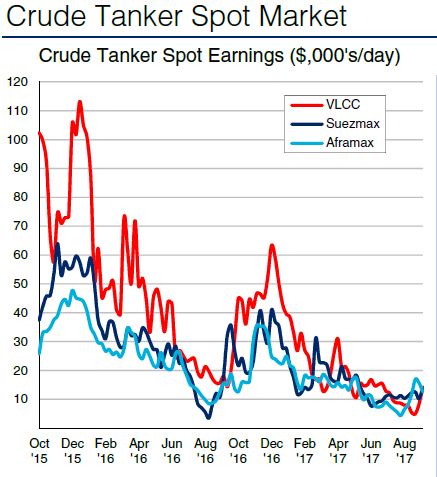

VLCCs

It was a busy week in the VLCC market, heavily aided by increased enquiry in the Atlantic on routes loading in both WAF and the Caribbean, with the rate on the WAF-China route firming to WS 60. The MEG also had another active week as charterers looked to get their cargoes fixed before the upcoming Golden Week break, with the Gulf-Japan route rising to end the week at WS 55.

Suezmaxes

Following a busy week in WAF where WS rates climbed into the 80s, the market paused slightly. However, the position list remains tight, suggesting these elevated rates could hold. Meanwhile, rates in the Med and East of Suez moved up modestly amid high levels of enquiry, with the Gulf-WC India route rate increasing to WS 75.

Aframaxes

Rates in the UKC/Baltic fell this week as charterers continued to put pressure on owners, with the Baltic-UKC rate falling to WS 82.5. Elsewhere, despite a busy week in the Med, rates generally slipped. Overall, average Aframax earnings weakened 19% w-o-w to $12,608/day.

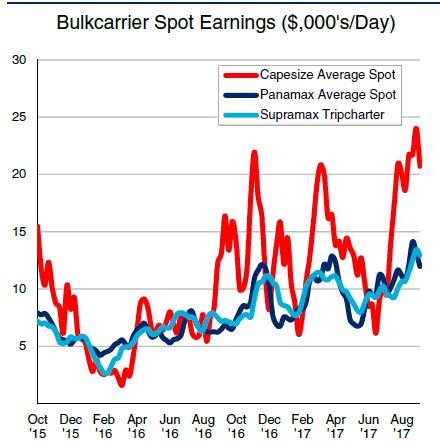

Bulkcarrier Highlight

Capesize

After rising firmly last week, Capesize spot rates eased this week, reflecting softening activity, particularly on routes out of Australia and Brazil. The spot rate on the Dampier-Qingdao route fell w-o-w to $7.45/tonne, while the rate on the Tubarao-Qingdao route fell to$18.25/tonne. Overall, average Capesize spot earnings fell 14% w-o-w to $20,723/day.

Panamax

Despite a steady stream of fresh cargoes out of NOPAC and S.E. Asia, long tonnage lists in the North Pacific and a shortage of coal cargoes out of Australia saw spot rates slide w-o-w in the Pacific basin. Meanwhile, limited fresh cargoes out of the US Gulf undermined spot rates in the Atlantic, despite shortening tonnage lists.

Handy

Reduced activity saw Supramax trip rates fall w-o-w in the Pacific basin. Meanwhile, sentiment has remained firm in the Atlantic, with rates generally increasing in the basin, despite a reduction in activity in the US Gulf.

Shipbuiding News

Rosneft has reportedly placed an order for 5 x 114,000 dwt ice class Aframax tankers at Russian yard Zvezda Shipbuilding.

The units are due for delivery from 2021. Earlier this year, Zvezda and Hyundai Samho formed a joint venture and signed a technical support agreement.

In the bulker sector, Hyundai HI has reportedly won a contract for 10 + 5 x 325,000 dwt ‘LNG-ready’ VLOCs from domestic owner Polaris Shipping. The vessels are backed by a long-term COA with Brazilian miner Vale and are due to be delivered from 2019. Shanghai Waigaoqiao has taken a contract from Foremost Maritime for 2 x 180,000 dwt Capesize bulkers. The units are due for delivery in Q42019. Meanwhile, Oshima Shipbuilding is reported to have received an order from Fednav for 6 x 34,500 dwt ice class1C Handysize bulkcarriers, due for delivery from 2019.

MSC has reportedly placed an order at Samsung HI for6 x 22,000 TEU boxships. The vessels are due for delivery in 2019. This follows an order placed by MSC last week at DSME for another 5 x 22,000 TEU containerships.

MSC has reportedly placed an order at Samsung HI for6 x 22,000 TEU boxships. The vessels are due for delivery in 2019. This follows an order placed by MSC last week at DSME for another 5 x 22,000 TEU containerships.

DSME for another 5 x 22,000 TEU containerships. Elsewhere, Jiangsu Fanzhou has placed an order at Nantong Xiangyu for one 60,000 dwt semi-submersible heavy lift vessel. The unit is due for delivery in 2019.