A Quote from Clarksons Regarding Shipping Industry

Clarksons in its weekly report offered an analysis regarding tanker, bulker, demolition and newbuilding market.

src="/files/fa/news/es/Thumbnails/7e766697-eb05-42a7-93cb-c3ff3a251a80_260_199.jpg' class='img_convert' title='A Quote from Clarksons Regarding Shipping Industry ' alt='A Quote from Clarksons Regarding Shipping Industry '>

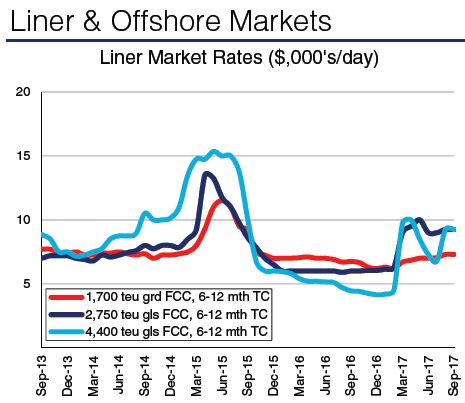

VLCCs

Whilst the supply/demand balance seems to remain weighted in charterers’ favour, owners have managed to push back a little this week. High activity in WAF last week attracted a large share of ballasters from the MEG, with tight tonnage supporting rates on ex-Gulf routes. Meanwhile, rates on routes ex-WAF also rose w-o-w, with the rate on the WAF-US Gulf route reaching WS 65.

Suezmaxes

Following a quiet start to the week, rates for vessels loading in WAF dipped below WS 65. However, this loading in WAF dipped below WS 65. However, this loading in WAF dipped below WS 65. However, this. However, this encouraged fresh cargoes and as a result rates firm slightly, with the WAF-Med route ending the week at WS67.5. Meanwhile, the Med/Black Sea market remained relatively quiet, although enquiry is beginning to pick up.

Aframaxes

High levels of activity kept rates buoyant at the start of the

week in the Black Sea and Med. However, these elevated levels discouraged charterers and rates began to ease.

Rates on featured Black Sea–Med and cross-Med routes fell w-o-w to WS 110 and WS 107.5 respectively.

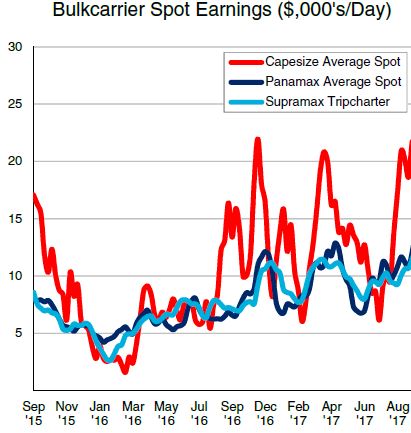

Bulker

Capesize spot rates rose firmly through the week, reflecting increased activity on routes out of W. Australia, Brazil and South Africa The spot rate on the Tubarao- Qingdao route rose w-o-w to $19.25/tonne. Overall, average Capesize spot earnings increased 11% w-o-w to a 3-year high of $24,018/day.

Panamax

Sentiment softened through the week in the Pacific, with Panamax spot rates falling despite a reasonable flow of cargoes out of NOPAC and E. Australia. Meanwhile, limited activity saw the spot rate on the Santos-Qingdao route fall w-o-w to $32.20/tonne. In general, long tonnage lists undermined spot rates across the Atlantic.

Handy

Average Supramax trip earnings rose 8% w-o-w to$13,438/day, as a continuous flow of fresh cargoes out of NOPAC and S.E. Asia supported rates in the Pacific. Meanwhile, tight tonnage in ECSA and firm activity in the US Gulf supported Supramax trip rates in the Atlantic.

A

the spot container freight rate on the Shanghai-US West Coast route stood at $1,484/FEU this week, a decrease of 6.4% from According to the Shanghai Containerized FreightIndex, $1,586/FEU last week. On the Shanghai-US East Coast route, the spot container freight rate stood at $2,105/FEU this week, down 7.2% compared rate stood at $2,105/FEU this week, down 7.2% compared to last week. Meanwhile, spot container freight rates on the Shanghai-North Europe and Shanghai-Mediterranean routes decreased by 4.6% and 2.9% week-on-week respectively, to stand at $734/TEU and $709/TEU.

Container throughput at the top five ports on the US West Coast (Long Beach, Los Angeles, Oakland and Seattle-Tacoma) stood at 2.1m TEU in August 2017, an increase of 5.7% y-o-y and representing the highest monthly throughput reported so far this year. In the first eight months of 2017, total box throughput at these ports stood at 15.0m TEU, up 6.8% relative to the same period of 2016.