says LLI

Crude Tanker Fleet to Growth

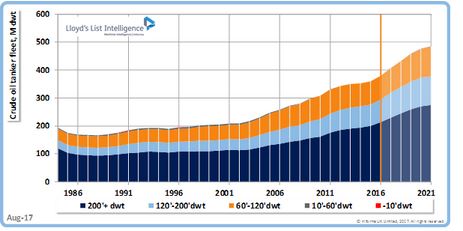

FLEET growth in the crude tanker sector will accelerate in the next five years owing to limited scrapping and a large orderbook, according to the latest forecast from Lloyd’s List Intelligence, sounding an alert for bullish market participants who predict an earnings recovery next year.

src="/files/fa/news/es/Thumbnails/4244b611-fdcd-4035-a3c1-9f5e271b75b3_260_199.jpg' class='img_convert' title=' Crude Tanker Fleet to Growth ' alt=' Crude Tanker Fleet to Growth '>

According to MANA, In the September Shipbuilding Outlook, LLI forecast an aggregate fleet growth of 27.7% in 2017-2021, which would almost double the expansion pace in the previous five years.

A total of 702 crude tankers with 133m dwt are due to be delivered in 2017-2021, the Shipbuilding Outlook said, while only 197 ships with 28m dwt will be scrapped.

“Only 42m dwt of the current crude oil carrier fleet was built before 2000. Removals until year-end 2021 will take place among those ships,” LLI said.

“Given the hefty fleet growth in the coming years, the market is bound to be subdued.”

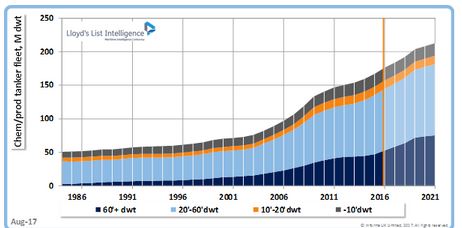

Meanwhile, the fleet of product carriers and product/chemical combined tankers is forecast to expand annually by 7.5% in 2017-2021,

versus an average of 3.7% each year in 2012-2016.

The segment of 60,000 dwt or larger is projected to expand annually by 7.5% in terms of capacity, while the smaller segments below 20,000 dwt will shrink.

LLI forecast the number of ships smaller than 10,000 dwt removed to be 144, which would be an all-time high historically.

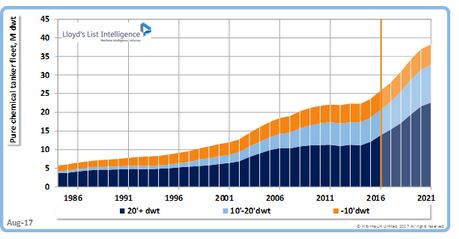

Elsewhere, LLI predicted the pure chemical fleet to grow 8.2% annually in 2017-2021 owing to a large orderbook, compared with an average annual rate of 3.1% in the previous five years.

As for gas carriers, LLI forecast the liquefied natural gas carrier fleet would expand by 7.6% over the next five years, versus 5% on the past five years.

“There is a heavy orderbook of 20.9m cu m – 30% of the current fleet. Therefore, the fleet will continue to grow,” the Shipbuilding Outlook said.

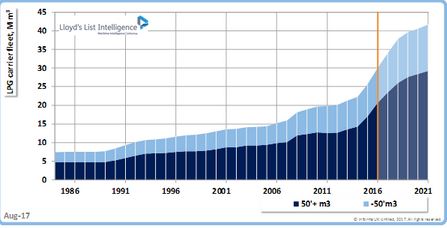

LLI also expected annual fleet growth in the liquefied petroleum gas sector to slow to 6.8% in 2017-2022 from 8.6% in the past five years, with more scrapping and limited newbuilding orders.